We explained impact of compounding in a previous article. There is one related concept called annuity which is critical to understand to plan for 30 years from now. This concept is vital when someone is planning for retirement income (pension) and hence have to be attached to NPS which mandate buying annuity at maturity.

Concept of Annuity is very counterintuitive at short durations but makes a lot of sense in longer term. Let me start by asking a simple question if at the beginning of an year you have 12000 Rs. How much are there for every month? Straight forward answer is 1000. but lets take this to long term. If at the beginning of retirement your corpus is 60 Lakh and you assume a post-retirement life of 20 years how much you can have for every year? I am sure you understand answer is not 3 lakhs (25k per month). You have just more than 6 lakh 30 Thousand (63k per month) per year*. Some of us might be thinking “Why?” and answer of this why is Interest and compounding. A good analogy of this system is like a farm house of chickens (For nitpickers among us, lets assume none of chickens die of natural death and every newborn is equally capable of reproduction. If only biological systems were as simple as financial systems) where you have put some chickens which grow by reproduction and you take few out every month for your household needs. No of chickens you take out are more than what they reproduce, so over a period of time you are going to run out of them. How long does it take before you run out of chickens is dependent on three factors:

- How many chickens were there initially

- Reproduction rate

- How many of them you take out

It may be difficult to model these factors for chickens but it is fairly easy for money and voila!! we have a financial product known as annuity. But this much is not enough, people responsible for managing money know, one size fits all approach do not work and hence they have made several tweaks and named them as different products.

- Some people want their mension to continue for their lifetime and hence do not want to touch the corpus while living and hand it over to kids after them. So they choose to get only interest as pension while on death the corpus is handed over to kids/relatives

- Some people might not want to take headache of moving their saving corpus from one product to another at retirement so may choose a single plan which takes care of investment while earning and provide pension after retirement. Bingo this is what traditional pension plans do

* Interest rate 8.75%. Give and take a few thousand based on interest calculation cycle

There are number of options available under the annuity category to cater to different needs and requirement. Like e.g. you may like your dependent to keep getting the full pension once you are not there or may want him/her to get 50% of the pension only after you, to cater to her needs only. Before exploring different kinds of product lets explore features first -

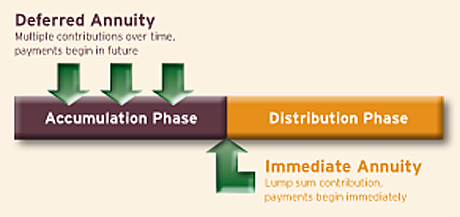

- Immediate or Deferred - If pension starts immediately after the purchase of annuity plan itself, its known as Immediate Annuity. In case annuity payouts (pension) starts after a certain period of annuity purchase or after you keep paying for annuity regularly for a period of time , its known as Deferred Annuity.

- Return/Non-Return of Capital - Whether the amount used to purchase the annuity is returned to the subscriber after ceasing of pension.

Now lets explore different kinds of Annuities one by one -

- Annuity for life - you receive pension for rest of your life

- Annuity for Certain Period - Annuity continues for a certain period decided at the time for subscription of the plan. In case of subscriber’s death in between the period , dependent gets the pension for the rest of the period. After the end of the period, pension ceases.

- Return of Capital - Purchase price of the annuity is returned to the dependent after death of the subscriber.

- Increasing Annuity - Pension increases at a certain rate every year

- Annuity with option for Pension for dependent -

- 50% Pension - Dependent gets 50% pension after the death of the subscriber

- 100% Pension - Dependent gets full pension after the death of the subscriber

- 100% Pension with Return of Capital - Dependent gets full pension after death of subscriber. After death of dependent of the subscriber, anybody nominated by subscriber gets the amount used to purchase the annuity.

Annuity as a product class is still in infant stage as far as India is concerned. Thanks to years of neglect by the government, greater penetration of other alternatives like PPF, absence of focussed marketing by Pension companies and lot many other factors. Pension companies not even disclose rates for different kinds of annuities at public platforms like websites etc. But as India moves towards to the path of a developed nation, Annuity as a product class is bound to grow substantially , as is the norm in developed nations.

No comments:

Post a Comment